for College

Watch This Before You Claim Your Roadmap

(Only 2:43 minutes)

If you’re an upper-middle-income or high-income parent, this short video is for you:

- There’s a college pricing trap most families do not see until it is too late.

- You may earn too much for most aid — but paying $40,000, $60,000, or $80,000+ per year still hurts.

In this short video, I’ll show you the Funding Gap, why it happens, and what to do next.

What You Get in Your $97 College Affordability Roadmap

not generic advice. It's built around your numbers!

1st - Quick Questionnaire

Complete this first so Peter can review your family’s numbers before your calls.

2nd - Prep Call

A short prep call to focus your Roadmap Session and answer key questions before the main session

3rd - Roadmap Session

Your 60–90 minute Zoom session with Peter. Both parents should attend if possible.

4th - Written Next-Step Plan

Delivered after your session, with your best next steps and colleges most likely to offer real money.

No more guessing. You’ll know your best next steps.

You’ll book your Zoom call right after checkout.

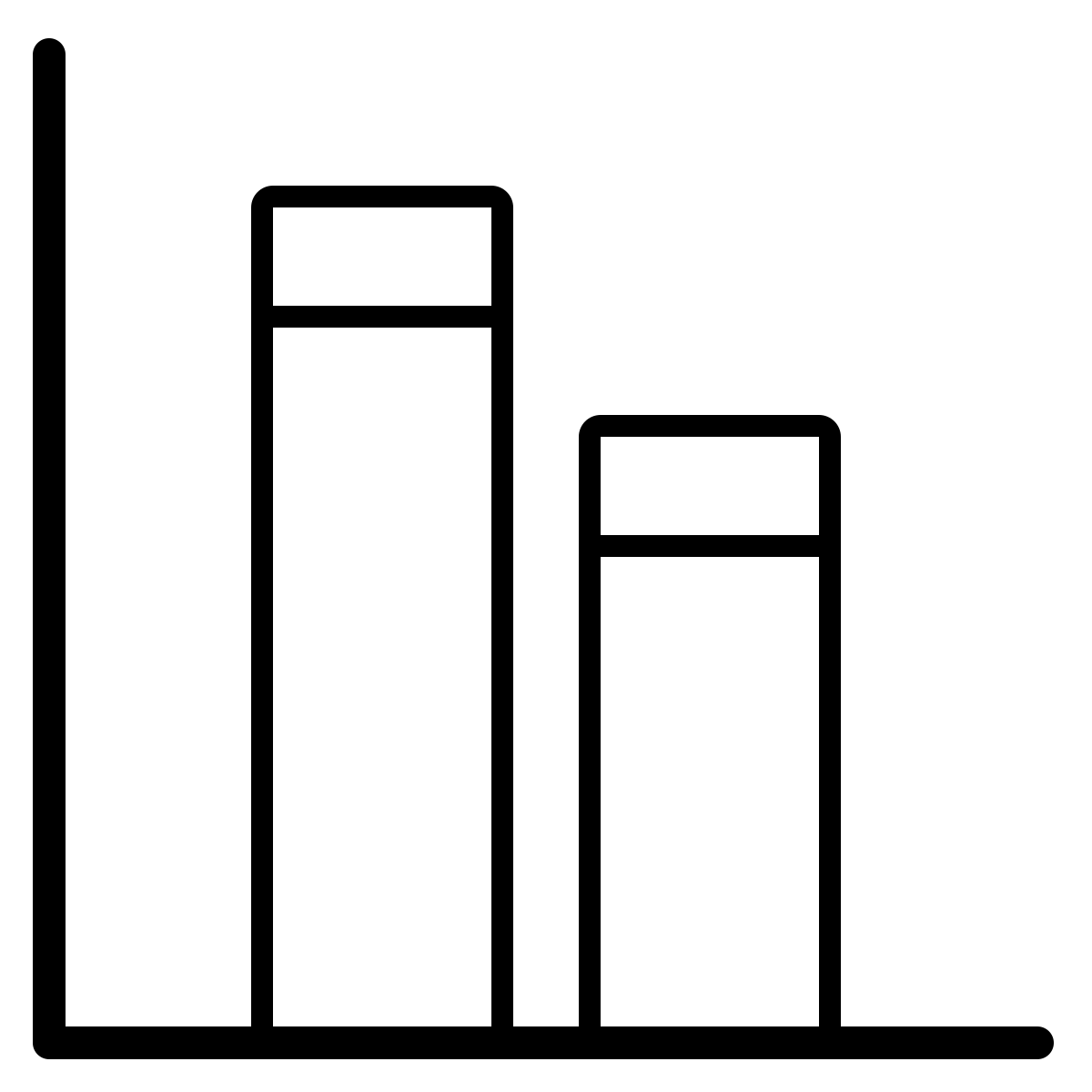

Reported Results

From 1,668 award letters submitted by families (2022–2025)*

Look at these savings, the difference between the sticker price and your net cost after grants/scholarships. This is money schools give out on purpose—if you know where to look.

Public Colleges

$34,480*

Average 4-year savings

(856 students)

Private Colleges

$107,983*

Average 4-year savings

(812 students)

All Colleges

$70,262*

Average 4-year savings

(1,668 students)

*Results vary by student and college. See FTC Disclosure below.

Total reported savings (2022–2025): $117,198,010*

Historical total (2009–2025): $2,233,119,514*

See FTC disclosure below for details.*

*Results vary by student and school. See FTC Disclosure below.

Want to see what’s realistic for your student? Claim your $97 Roadmap.

What We’ll Cover in Your Roadmap Session:

Your best next moves—how to lower your real college cost based on your numbers

College list strategy —which colleges may be more likely to offer real money

Merit + need-based strategy—what’s realistic for your student

Financial aid forms, FAFSA/CSS positioning—the biggest mistakes that can quietly raise your cost

Your action plan—what to do first, second, and third

- This is a planning call, not a pitch

- You’ll leave with clear next steps

- You’ll get your written next-step plan after the session

- If we’re not a fit, I’ll tell you

Both parents should attend if possible so you can make clear decisions together.

Right after checkout, you’ll complete a short questionnaire and book your prep call.

I'm Peter Lampert—attorney, CPA, and father of three college graduates

I help families lower college costs before the bills hit.

When my oldest was getting close to college, I was scared.

Like many parents, I had saved, planned, and earned a good income — and still felt stuck in the financial aid dead zone.

I did not want to drain our retirement. And I did not want to limit my children’s options.

So I got to work.

I studied the FAFSA, the CSS Profile, and the financial aid strategies colleges use to decide who pays more and who gets real help.

What I learned changed everything.

All three of my children attended great private colleges for less than our in-state public option would have cost.

That is the work I do with families now.

Credentials & Background:

Education: UVA, Boston University, University of Nebraska, NYU Law

Licenses: CPA, Attorney

Affiliations: AICPA, ABA, NCAG, HECA

Four Quick Examples of How Families Lowered College Costs

Small changes in school choice, aid strategy, and timing can change what a family pays by tens of thousands.

Julie: The dream school cost less than the big in-state “safe” plan

Community college plus the in-state option looked cheaper. They were not—after aid.

Result: Emerson came in $24,000 less than the “safe” plan.

Takeaway: The lowest sticker price is not always the lowest real cost.

Sarah: She got in — then we closed the money gap

She was admitted to Ithaca, but the first offer did not make it affordable.

Result: Her cost dropped to match the in-state public option — saving $100,000+ over four years.

Takeaway: A first offer is not always the final offer.

High-income families: Merit aid still shows up

Need-based aid may be limited. But merit aid is based on how much a college wants your student.

Result: Many higher-income families still get real discounts by targeting the right schools.

Takeaway: It’s not just what you make. It is also where your student is most wanted.

My family: 3 kids. The sticker price was almost $1,000,000

We used positioning, smart school choices, and negotiation.

Result: Total cost came to $421,866 — a 58% reduction and $41,000 less than the “safe” public option — without touching retirement.

Takeaway: This is how the system works in real life.

Want to see what’s realistic for your student? Claim your $97 Roadmap

Questionnaire + Prep Call + 60–90 minute Roadmap Session + Written Next-Step Plan

Both parents should attend.

Is This College Affordability Roadmap Right for Your Family?

Best fit for your family if:

- Student is in 8th–11th grade (or early 12th grade)

- Household income is roughly $150,000–$400,000+

- Open to schools beyond just brand names

- Both parents can attend if possible

Probably not the best fit if:

- You only want scholarships and won’t change your plan

- You only want Ivy/Top 20 schools (and won’t consider others)

- You are not willing to share basic numbers

- You are not ready to act a clear pland

Ready to get your College Affordability Roadmap?

Start with the $97 Roadmap and leave with clear next steps

Questionnaire + prep call + 60–90 minute Roadmap Session + written next-step plan

Normally $750

Today: $97

Get your Roadmap. Stop guessing!

Normally $750. Tonight: $97.

- 1st — Quick Questionnaire

- 2nd — Prep Call

- 3rd — 60–90 Minute Roadmap Session

- 4th — Written Next-Step Plan including college list targets where real money is more likely to show up

Available appointment slots in the next two weeks are limited.

Next step: Checkout → complete your questionnaire → book your prep call.

Book your $97 College Affordability Roadmap and receive:

- 60–90 Minute Roadmap Session with Peter Lampert (CPA + attorney)

- FAFSA/CSS strategies to avoid mistakes that quietly raise your cost

- College list targets where real money is more likely to show up

- Retirement protection strategies so college does not wreck your retirement

- Written Next-Step Plan with your best next steps, in order

Both parents should attend if possible.

You’ll book your prep call right after checkout.

You’ll leave with clear next steps you can use right away.

If you complete the session and do not feel you received $97 in value, we’ll refund every penny.

Claim your $97 College Affordability Roadmap offer while spots are still open.

After that, the price returns to $750.